How Do Financial Advisors Earn Money?

Most people don’t ask their financial advisor how they get paid. That's a problem, because compensation structure is a strong predictor of the advice you'll receive.

Here's how the four main models work and what each one means for you.

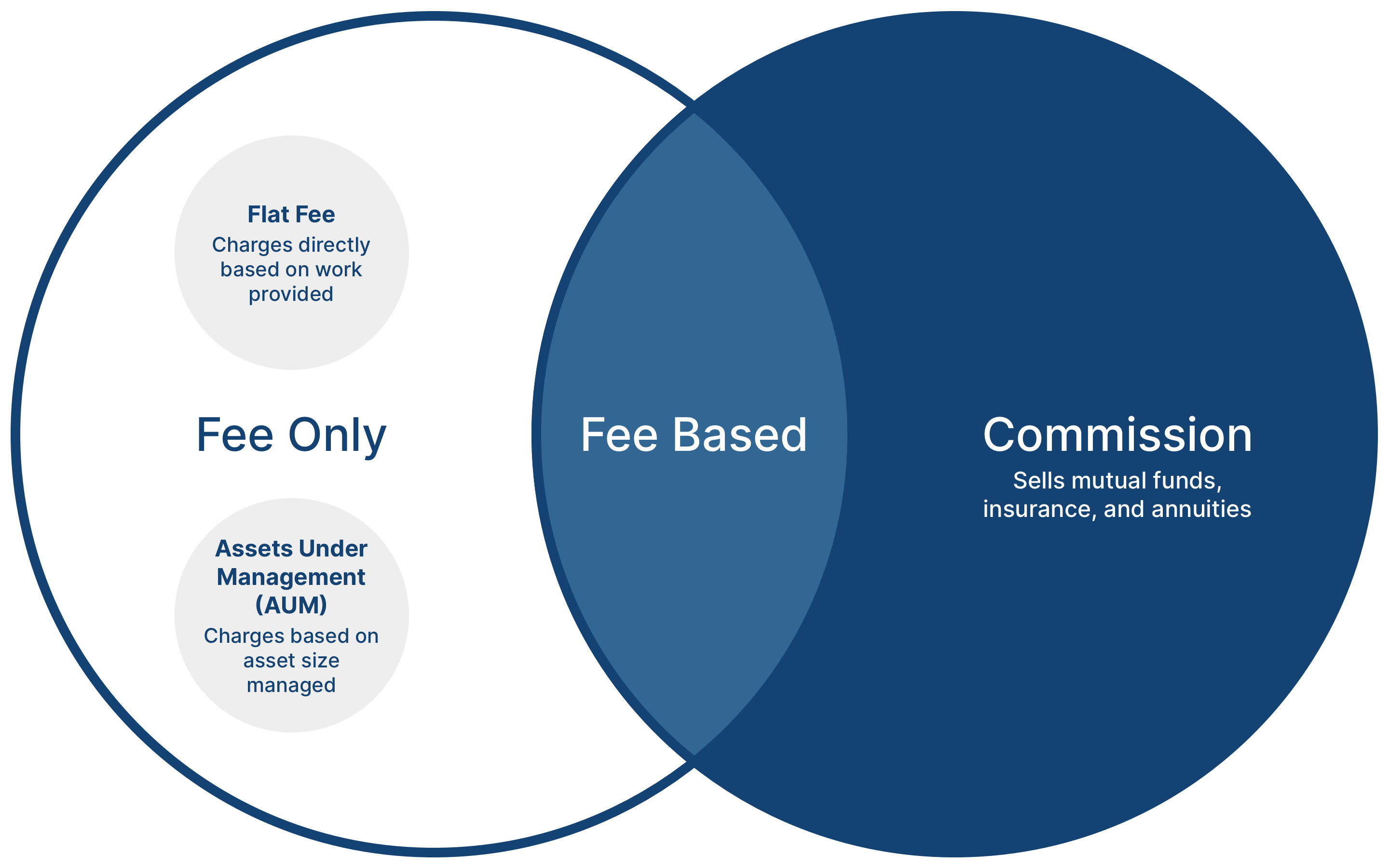

Flat Fee, Fee-Only Advisors

Flat fee advisors charge based on the work they provide. Fees may be structured as hourly rates, monthly or annual subscriptions, or one-time project fees. Their income has no connection to product sales or portfolio size.

This model has the fewest conflicts of interest of any compensation structure. When an advisor's fee is fixed, their incentive is to do good work. Full stop.

Flat fees are also the most transparent. You know exactly what you're paying before you engage.

Assets Under Management (AUM) Advisors

AUM advisors charge a percentage of the assets they manage, typically around 1% per year. As your portfolio grows, their fee grows with it, regardless of whether the scope of their work increases.

The math compounds quickly. On a $1 million portfolio earning 7% annually, a 1% AUM fee costs roughly three times more over 20 years than a flat fee advisor charging $6,500 per year. On a $5 million portfolio, that difference exceeds $2.5 million.

This model can also create subtle incentives that don't serve your interests:

- Just because you work hard to make more and save more doesn't mean their workload increases, but their fee does

- Recommending rollovers of 401(k) or 403(b) accounts into managed accounts increases their fee

- They may not recommend paying off high-interest debt because that reduces the assets they manage

- They may steer you away from real estate or other investments held outside their management

- It's easier for them to grow revenue by acquiring new clients than by improving returns, so existing clients can become an afterthought

Commission-Based Advisors

Commission-based advisors earn money by selling financial products such as insurance policies, annuities, and mutual funds. They may not charge you a direct fee at all, but they are compensated by the companies whose products they recommend.

This model carries the highest potential for conflicts of interest. Recommendations can be shaped by commission structures rather than your financial situation. Products with higher commissions include whole life insurance, universal life policies, variable annuities, and actively managed mutual funds with high expense ratios. They may also be incentivized to move funds out of retirement accounts to purchase these products.

Commission-based advisors are not fiduciaries. They operate under a suitability standard, meaning recommendations only need to be suitable for you, not the best available option.

Fee-Based Advisors

Fee-based advisors are a hybrid. They charge advisory fees and earn commissions on products they sell. This is not the same as fee-only.

The distinction matters. A fee-based advisor may act as a fiduciary in some parts of your relationship and not others. When recommending a product that generates a commission, they may not be required to act in your best interest. Always ask specifically whether they are a fiduciary at all times, not just sometimes.

Flat Fee

- Charges a fixed rate: hourly, monthly, or per project

- Fee has no connection to product sales or portfolio size

- Fewest conflicts of interest of any compensation model

Assets Under Management (AUM)

- Charges ~1% of your portfolio annually typically

- Fee grows as your balance grows, regardless of workload

- May discourage paying off debt or investing outside their management

Commission-Based

- Earns money by selling financial products, not charging you directly

- Compensated by the companies whose products they recommend

- Higher-commission products may be prioritized over better options for your situation

Fee-Based (Hybrid)

- Charges advisory fees and earns commissions on products they sell

- Not the same as fee-only, despite similar-sounding name

- The line between advice and sales can be blurry

How to Verify How Your Advisor Is Paid

All registered investment advisors are required to file a Form ADV with the SEC or their state regulators. This document discloses their fee structure, compensation sources, and any potential conflicts of interest. You can look up any advisor at adviserinfo.sec.gov.

Before hiring any advisor, ask these questions directly:

- Are you fee-only or fee-based?

- Do you earn commissions on any products you recommend?

- Are you a fiduciary at all times?

- Can I see your Form ADV

A straightforward, confident answer to all four is what you're looking for.

Why This Matters More Than You Think

Compensation structure shapes behavior, even for well-intentioned advisors. The question is not whether your advisor is a good person. It's whether their incentives are aligned with yours.

Flat fee, fee-only advisors earn their income entirely from the fee you pay them for their work. No commissions. No percentage of your portfolio. No reason to recommend anything other than what's best for your situation.

Want to work with an advisor whose only incentive is your financial wellbeing?

Find a Flat Fee Advisor